Knowing your credit score helps you judge which loan products might approve you. With a credit score above seven hundred forty, you qualify for the best rates. Between six hundred eighty and seven hundred thirty nine, you can still get good rates, though not necessarily the best. Between six hundred twenty and six hundred seventy nine, you may only get higher rates. Below six hundred twenty, traditional loans may be hard to get, and you should consider secured loans or credit unions.

The second step is determining exactly how much you need to borrow. Borrow only the amount you need. Do not borrow more just because the lender approves a higher amount. Every extra dollar you borrow is a dollar plus interest you must repay. Calculate the precise number you need, and apply for only that number.

The third step is choosing the right loan type. If you need a small amount, say five hundred to five thousand dollars, a personal loan or credit card may be appropriate. If you need a medium amount, five thousand to thirty thousand dollars, a personal loan, credit union loan, or secured loan is more suitable. If you need a large amount, above thirty thousand dollars, a home equity loan or home equity line of credit is a common choice, but you need to own a home.

The fourth step is comparing multiple lenders. Do not go only to the bank where you have your checking account. Online lending platforms, credit unions, community banks, and national banks can have very different rates and terms. Compare at least three. Compare annual percentage rates, fees, repayment terms, and monthly payments.

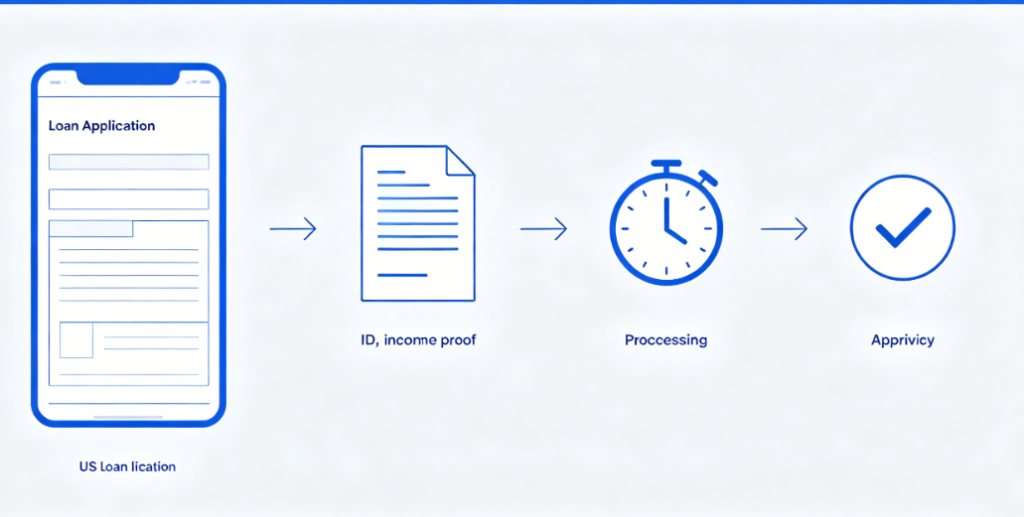

The fifth step is preparing your application materials. Having these ready in advance greatly speeds up the process. Typical required materials include a government-issued ID, Social Security number, proof of income, employment information, and information about existing debts. If your income comes from self-employment or non-traditional sources, you may need additional documents such as bank statements or tax returns.

The sixth step is submitting the application. Online applications are typically the fastest, taking just minutes to complete. Some lenders offer instant approval decisions. Others take a few hours or days. If you need money very quickly, choose a lender that offers instant approval. But be aware that instant approval often comes with a slightly higher interest rate.

The seventh step is reading the terms carefully after approval. Do not skip reading the contract just because you need the money urgently. Confirm whether the interest rate is fixed or variable. Confirm whether there is a prepayment penalty. Confirm whether there are other fees. Confirm the monthly payment amount and due date.

If you want to get a loan quickly, certain things will slow you down. Providing incomplete information is the most common cause. Make sure all information is accurate when you apply. Applying outside of business hours can also cause delays, as some lenders require human review. Applications submitted on weekends and holidays typically take longer to process.

Finally, be wary of loan advertisements that say “guaranteed approval” or “no questions asked.” These are often from predatory lenders. Their interest rates are extremely high and their terms are harsh. Getting a loan quickly is not worth taking on debt that will take you years to repay. If you need money but cannot get it from legitimate sources, better options include asking family for help, negotiating a repayment plan with creditors, or seeking help from a non-profit credit counseling agency.

Getting a loan correctly means you understand what you are signing. Getting a loan quickly means you have prepared your materials, chosen the right lender, and had a smooth application process. Combining both requires some preparation, but it is worth it.