- The Core Concept: An “Anti-Insurance” Product Life insurance solves the risk of dying too soon – your family gets money when you’re gone. An annuity solves the risk of living too long – you’re still alive, but your money runs out.

Simple definition: You sign a contract with an insurance company. You pay a lump sum or a series of payments. In return, the insurer promises to pay you a stream of income starting now or in the future. The payments can last for a set number of years or for your entire lifetime – no matter how long you live.

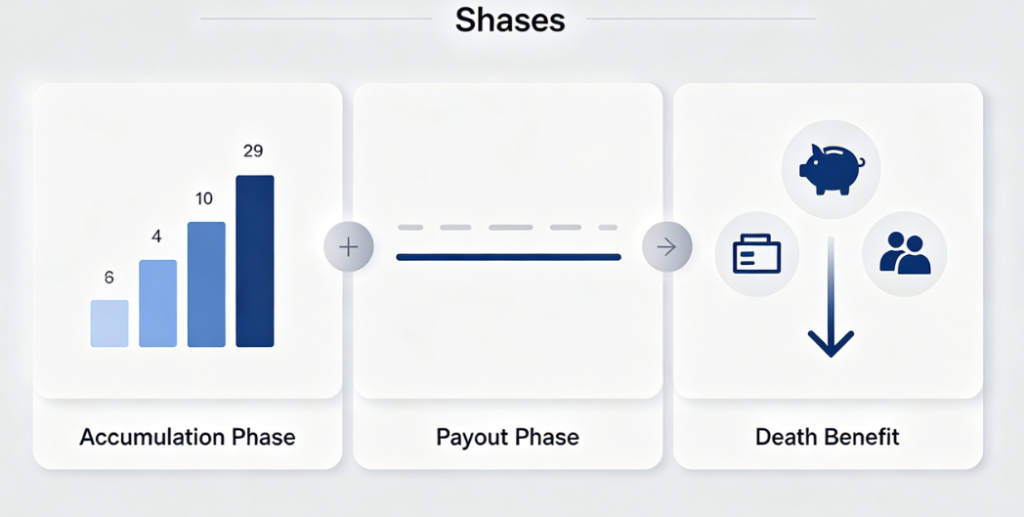

- The Two Phases: Accumulation vs. Payout Every annuity has two distinct phases:

Phase Explanation Accumulation You put money into the annuity. It grows tax-deferred (similar to a 401(k), but with no annual contribution limit) Payout (annuitization) The insurance company starts sending you regular income. Once you annuitize, you generally cannot get your lump sum back Not everyone annuitizes. Many people use annuities as tax-deferred investment accounts and withdraw as needed. But the core promise of an annuity is guaranteed lifetime income.

- Three Main Types of Annuities Fixed Annuity The insurance company guarantees a minimum interest rate. When you start taking income, the payment amount is fixed.

Pros Cons No market risk Low returns (slightly above Treasuries) Principal protected Inflation risk – same dollars buy much less in 30 years Predictable income Surrender charges for early withdrawal Variable Annuity You allocate money to sub-accounts (similar to mutual funds). Your returns – and future income – go up or down with the market.

Pros Cons Higher growth potential Can lose principal in a down market Tax deferral High fees (2%–3% per year) Some have downside protection Complex and hard to compare Fixed-Indexed Annuity (FIA) A hybrid. Your return is tied to a stock index like the S&P 500, but with a guaranteed floor (typically 0%–1%). You participate in some upside, but usually with a cap (e.g., the market rises 20%, but you only get 6%–8%).

Pros Cons Principal protection Caps limit your gains Participation in market upside Long surrender periods (7–10 years) Lower fees than variable annuities Complex terms, hard to compare across companies (AFS ad: fixed-indexed vs. variable annuity guide)

-

Immediate vs. Deferred Annuities Type When Income Starts Best For Immediate annuity Within 12 months of purchase Someone already retired who needs income now Deferred annuity 1+ years (often 5–20 years later) Someone still working who wants tax-deferred growth Example: A 65-year-old buys an immediate fixed annuity with $200,000. The insurer might pay $1,100 per month for life. A 50-year-old buys a deferred variable annuity and lets it grow until age 65, then converts to income.

-

Fees You Must Know: Annuities Aren’t Free Annuity fees are much higher than mutual funds or index funds:

Fee Type Typical Range Mortality and expense risk charge 1.0%–1.5%/year Administrative fee 0.1%–0.3%/year Optional riders (e.g., death benefit) 0.5%–1.0%/year Surrender charges (first 5–10 years) 5%–10% Comparison: An S&P 500 index fund has an expense ratio of just 0.03%–0.10%. Annuities can cost 10 to 100 times more.

- Tax Rules: Deferred, Not Tax-Free Your contributions are made with after-tax dollars (unless the annuity is inside an employer retirement plan)

Money grows tax-deferred during accumulation

When you withdraw: Withdrawals are considered earnings first (taxed as ordinary income); principal is not taxed again

Important: Withdrawals before age 59½ incur a 10% penalty on top of regular income tax.

- Riders: Valuable or Overpriced? Insurance companies sell optional riders. Common ones include:

Rider What It Does Worth It? Guaranteed lifetime withdrawal Keep receiving income even if account value goes to zero Valuable for conservative investors Death benefit Beneficiaries get at least your principal back Cheaper to buy term life insurance instead Inflation protection Income adjusts with CPI Very expensive, rarely worth it Expert advice: Most riders are overpriced. If you need lifetime income, prioritize a guaranteed lifetime withdrawal rider. Skip most others.

(AFS ad: long-term care insurance, retirement tax planning)

- Alternatives to Annuities – You Might Not Need One Before buying an annuity, consider these alternatives:

Delay Social Security: For each year you delay (ages 60–70), your monthly benefit increases by about 8%. This is the best inflation-adjusted lifetime annuity available

Bond ladder: Buy Treasuries with different maturity dates that roll over. Almost zero fees

4% rule: A 60/40 stock/bond portfolio, withdrawing 4% annually. Historically, a 90%+ success rate over 30 years

Dividend stocks/REITs: Generate cash flow with growth potential

- Who Is Actually a Good Fit for Annuities? Good Fit Poor Fit Worried about outliving savings to age 95+ Under age 60 with earned income No other guaranteed income (pension, etc.) Healthy and able to keep working Extremely low risk tolerance Wants to leave a large inheritance Already maxed Social Security and pension Capable of self-managing an investment portfolio

- Checklist Before Buying an Annuity Have I maximized my Social Security benefits (delayed to 70)?

Have I used all my 401(k) and IRA tax-deferred space?

Am I willing to lock up money for 5–10 years without touching it?

Do I understand all fees and riders?

Have I compared quotes from at least three insurance companies?

Have I consulted a fee-only financial advisor (not a commission-based seller)?

Conclusion Annuities are neither evil nor a miracle cure. They are a financial tool – useful in the right context, expensive in the wrong one. Annuities are best used to convert a portion (not all) of your retirement savings into lifetime income as a supplement to Social Security and pensions. But always understand all fees and terms before buying.