Part 1: How Buy Now, Pay Later Works Buy now, pay later is not a credit card. It’s also not a loan – at least not a traditional one.

It’s a short-term installment plan. The most common model is “four payments.”

Typical process:

You select furniture. At checkout, you choose the buy now, pay later option. You pay the first payment – typically a quarter of the total. Then you take the furniture home. Every two weeks, you pay another quarter. After six to eight weeks, it’s paid off.

No interest during this time. As long as you pay on time.

Key difference: Credit cards let you roll debt. Buy now, pay later forces you to pay off quickly.

Part 2: Why Merchants Like It Merchants promote buy now, pay later not out of kindness. Because it makes you spend more.

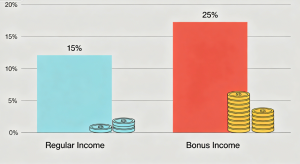

Studies show people spend twenty to thirty percent more on average when using buy now, pay later versus credit cards. Because installment payments dull price perception.

A $1,000 sofa looks expensive. But “pay $250 now, then $250 every two weeks” looks cheap. The total is the same. But your brain processes it differently.

Merchants are willing to pay the cost. They pay the buy now, pay later company three to six percent of the transaction. But they’re willing because your order is larger.

Part 3: Why Consumers Like It First, you don’t need the full amount upfront. This is the most obvious benefit.

Second, many plans don’t check credit. If you have no credit history or low credit, buy now, pay later might approve you when a credit card won’t.

Third, no interest (if you pay on time). Credit cards, by contrast, start charging interest from the purchase date if you don’t pay in full.

Fourth, the application process is fast. A decision in minutes.

Fifth, it can help build payment history. Some buy now, pay later companies report on-time payments to credit bureaus.

Part 4: Where the Risks Are Risk one: late fees

If you miss a payment, the company charges a late fee. Typically a few dollars to around fifteen dollars. Not huge. But if you miss repeatedly, fees add up.

Some companies also restrict your future access to their service.

Risk two: you buy what you can’t afford

Because each payment looks small, you might buy multiple furniture pieces. One piece at fifty dollars a month. Another at forty dollars a month. A third at thirty dollars a month. That’s one hundred twenty dollars a month. Then you forget the total until bills arrive.

Risk three: returns are complicated

When returning furniture, buy now, pay later is more complex than credit cards. You need to coordinate with both the merchant and the buy now, pay later company. Your refund may not automatically return to your account. You might wait weeks.

Risk four: automatic payment issues

Most buy now, pay later plans require linking a debit or credit card for automatic payments. If your account balance is low, you might incur bank overdraft fees.

Part 5: Furniture-Specific Considerations Buying furniture is different from buying clothes. With clothes, you know the same day if they fit. With furniture, you discover problems after it’s in your home.

Issue one: wrong size. It looked right online. At home, it’s too big or too small.

Issue two: wrong color. Screen colors and real colors are different.

Issue three: quality issues. Cheap furniture breaks after a few months.

If you buy furniture with buy now, pay later and need to return it, the process is:

You contact the merchant to request a return. The merchant agrees. The merchant notifies the buy now, pay later company. The company cancels remaining payments and refunds what you’ve already paid. This takes days to weeks. During this time, you might still be charged.

Advice: Before buying furniture, try to see it in person. Measure your space. Read the return policy. Then decide which payment method to use.

Part 6: How to Use Buy Now, Pay Later Safely Principle one: one plan at a time

Don’t use three or four buy now, pay later plans for different items at the same time. The total payments quietly add up.

Principle two: set reminders

Mark each payment date on your calendar. Or turn on automatic reminders from the buy now, pay later app.

Principle three: test with a small amount first

If you’ve never used a particular buy now, pay later service, buy one cheap item to test. Learn how they charge, how they notify you, how fast customer service responds.

Principle four: read the terms

Find answers to two questions: How much is the late fee? What happens if I return the item?

Principle five: don’t use it for things that lose value quickly

Furniture loses value. The day you buy it, it’s worth half. This isn’t a buy now, pay later problem. It’s a purchase decision problem. But buy now, pay later makes that decision easier to make – not necessarily better. Conclusion Buy now, pay later is a tool. Not good. Not bad. It depends on how you use it.

Use it for things you were already going to buy and can pay off within six weeks. Don’t use it for things you’re buying just because “the payment looks small.”

Furniture is part of your home. It deserves careful consideration. The payment method is just the last step. Choose the right furniture first. Then choose the right way to pay.